How the Level of Interest Paid in an Economy Influences European Banks Net Interest Income and Provision Outlook

Since 2008, total household debt has risen by 40% in absolute euro terms in Germany. In France, it is +80%, the Netherlands (+30%), Belgium (+90%) and Austria (+42%). It is down by 36% and 22% in Ireland and Spain, respectively. The leverage mix has also changed in every country, with a greater proportion of mortgages in the loan stock. Growth in higher cost unsecured consumer finance has been more limited since 2011.

Total interest paid has fallen sharply in every region. This reflects the decline in average household loan rates. For example, in Italy, it is now only 2.4%, down from 6.4% in 2008. Consequently, the annual household interest bill has fallen from €40.6bn to €18.9bn (-53%). Indeed, the decline in interest paid to the banks is even more severe in regions where debt was reduced. It is down -65% and -70% in Ireland and Spain, respectively. This period was a very bearish backdrop for European bank net interest income.

Household incomes rose sharply across every geography, particularly since 2011. This is due to both higher employment and wages. Discretionary spending power (HDSPTM)also surged, even allowing for higher essential item inflation in the 2019-2022 period.

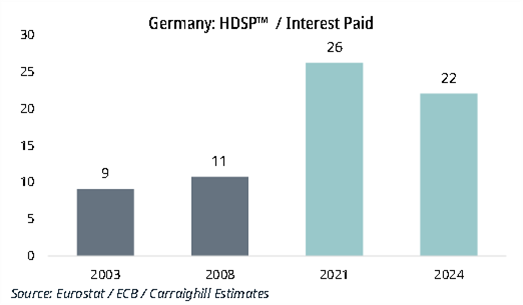

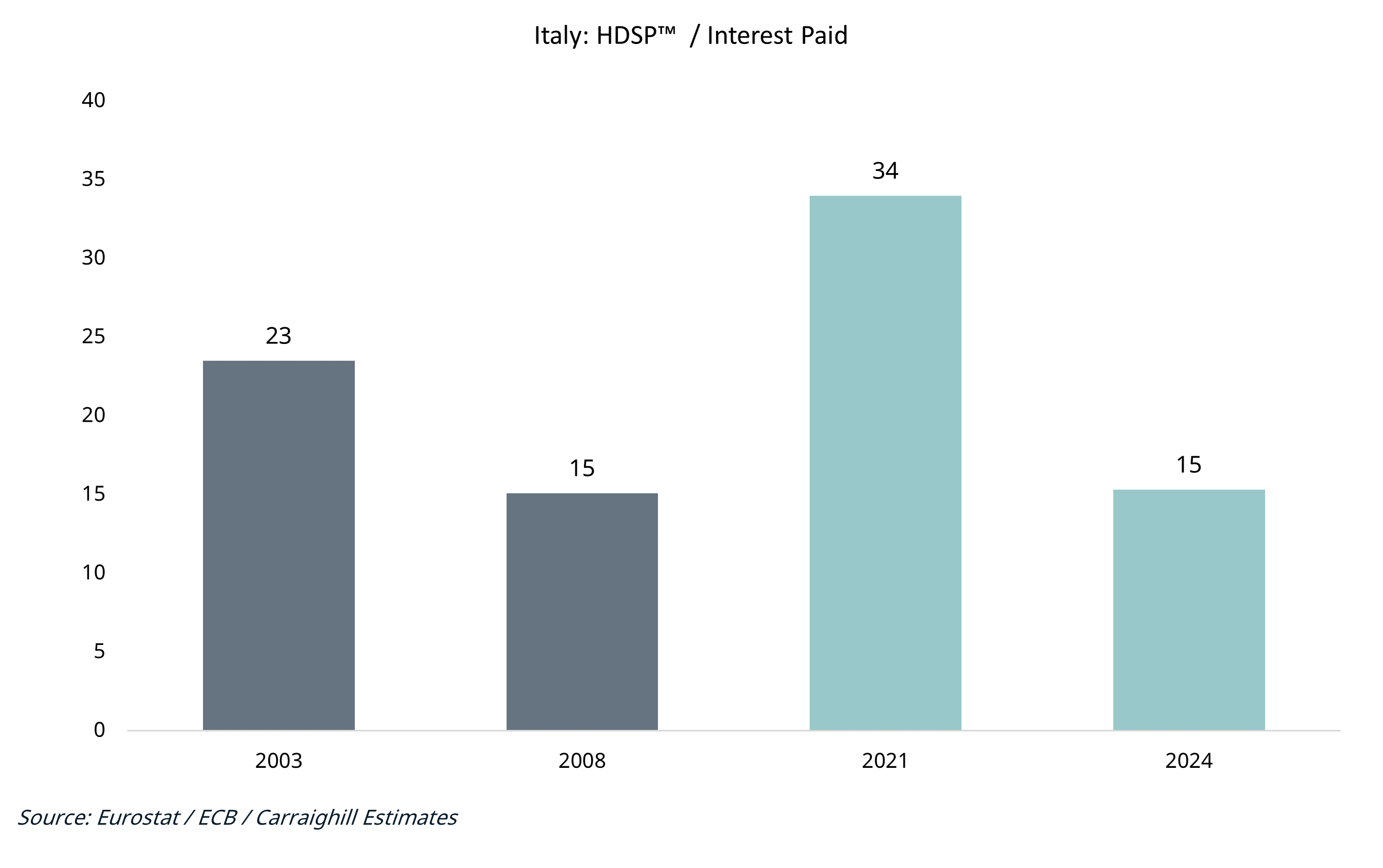

Reflecting the evolution of these key numbers, the household interest coverage ratio rose sharply. For example, in Spain, the ratio of HDSPTM to interest paid moved from 8x in 2008 to 27x at the end of 2021. It is now close to 30x in Germany, France, and Italy. This is over 100% higher than its 2008 level.

This high interest coverage level helps explain the lack of loan losses in the banks to date (households have significant levels of excess cash flow to cover interest).

However, this is going to change as higher interest costs flow through household cash flows. The key determining factors include:

The front book loan rate: The higher the front book loan rate the larger the impact on consumers. This varies by country.

The duration of the loan stock: In Italy it is only 2 years, whilst it Germany it is 7 years. This means that the impact on Germany households will be slower.

The coverage ratio in Italy rose from 15x to 34x from 2008 to 2021. It will fall to 15x by 2024f.

The ratio in Germany rose from 11x to 26x but should only fall to 22x by 2024f.

We have completed this analysis for all European countries and the UK. The discrepancies are large.

What does it mean? It has implications for European banks net interest income, customer spread, loan loss provisions. It also has consequences for asset management firms as household cash flow is diverted away from savings products towards servicing interest.

Carraighill’s work involves deep concentration on data to understand the environment within which banks, asset management, payment and REITs operate in Europe and select emerging markets. We also do bottom-up fundamental work on close to 50 companies across these sectors. If you would like to speak to us on the topics raised in this piece, you can contact us here.