European Energy Crisis: Causes and Consequences

Europeans are set for a cold, costly winter this year. The ongoing energy crisis shows little sign of easing, while the headline inflation rate accelerated to 4.1% in October. In our view, these price pressures are cyclical. Large debt overhang, weak demographics, and faltering productivity should ultimately lead to a further decline in long-term interest rates.

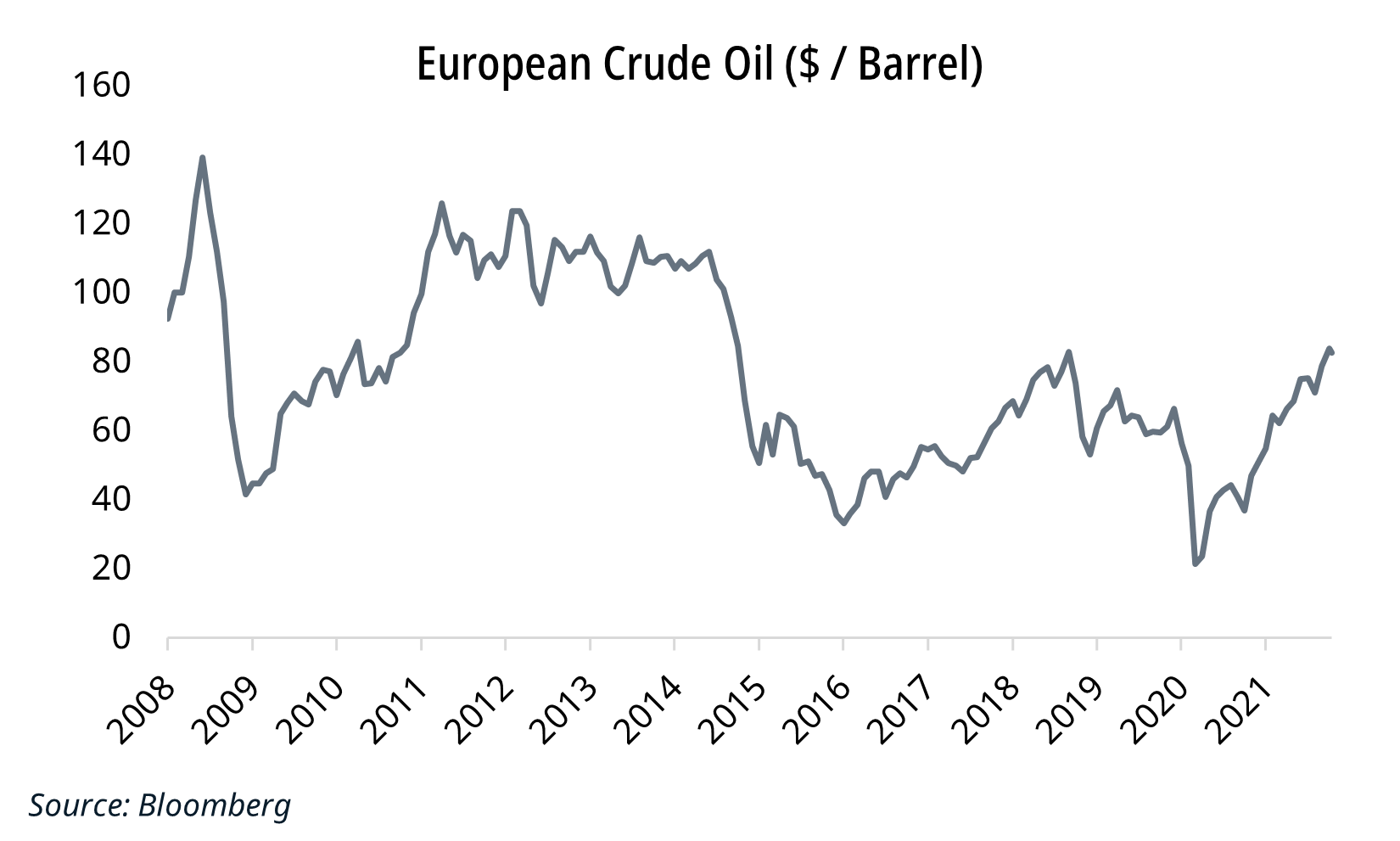

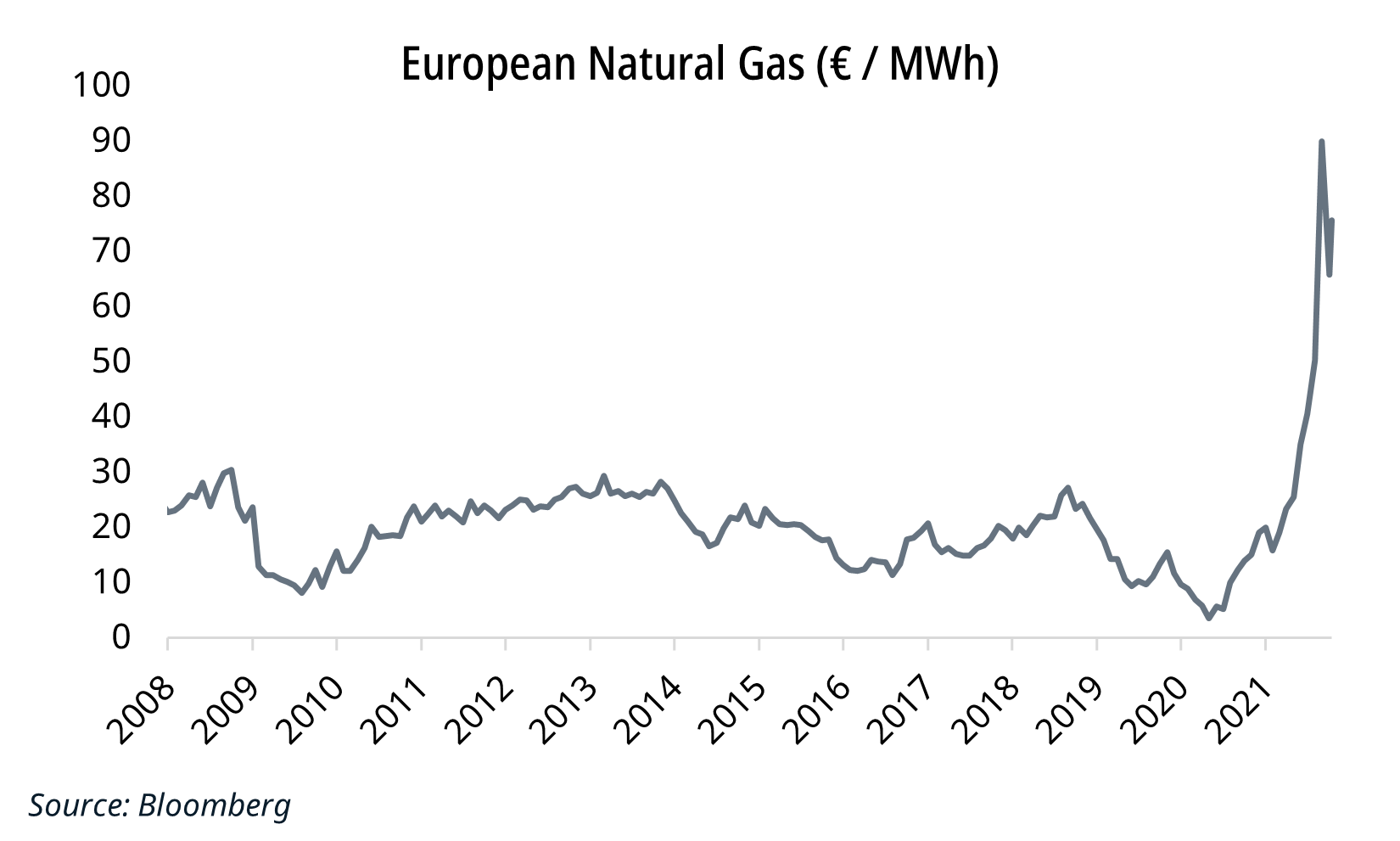

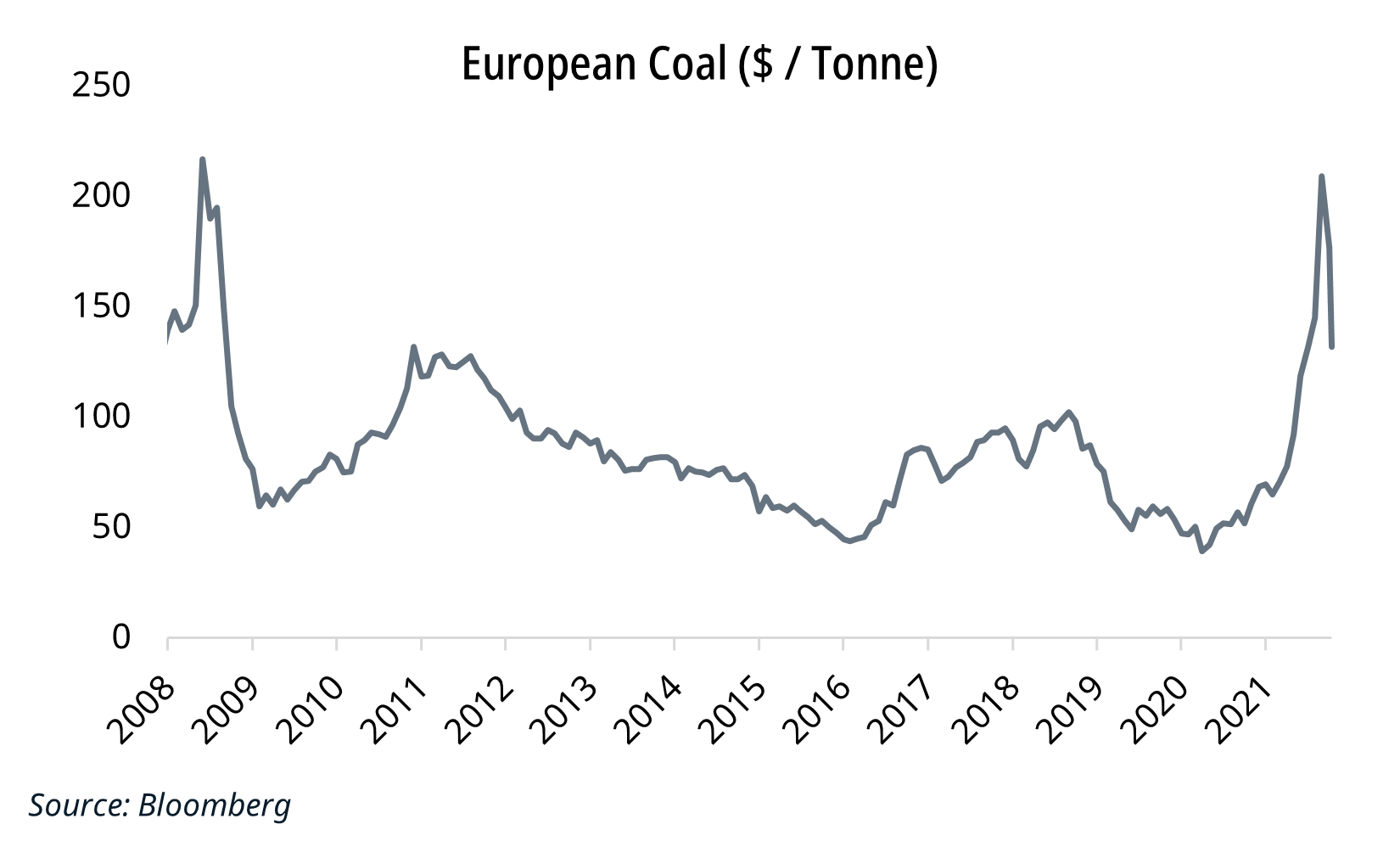

Yet, the current period of high inflation can’t be ignored. Food and energy bills are rising for households. Natural gas has increased nearly 3-fold, while oil and coal have increased 62% and 93% YTD, respectively. The EU remains reliant on global trade for its energy needs. 90% of natural gas is imported (40% from Russia). The cause of these price rises has been highly publicised, including the following:

- Demand: The broad reopening of the economy has unleashed exceptional demand. This was driven by extensive government supports and high household savings throughout 2020. This heightened demand for goods (rather than services) This surge may be temporary, but consumers’ stock of savings remains high.

- Supply: This surging demand continues to outpace rebounding global supply. Supply bottlenecks are primarily related to COVID-19 restrictions and additional checks globally. This has driven commodity prices higher whilst labour shortages are influenced by temporary furlough schemes. As a consequence, the participation rate has fallen in most global economies. Tempting these workers back will be important.

- Green transition: Low wind speeds and dry conditions reduced renewable energy generation over the past year, which has increased reliance on carbon-intensive sources. This was also particularly evident in higher demand for natural gas away from The EU has largely failed to bridge the transition from traditional fuels to cleaner energy. Lower output has reduced inventories at energy storage facilities. It is now too late to boost supply through the winter months.

These issues cannot be solved quickly and are unlikely to normalise for quite some time. This historic surge in energy costs continues to drive price pressures through the economy. From a macroeconomic perspective, we aim to understand these developments on a global scale.

- Government response: Public finances are likely to bear the brunt of the ongoing energy crisis. Various measures have been introduced to reduce the impact on households. This includes price caps, subsidies, and a reduction in tariffs. For example, Italy is set to spend €5bn to ease the impact of rising prices on consumers. These policies come when public debt is at historic levels, and EU politicians are calling for a return to strict fiscal rules. This higher spending is a temporary fi It is unlikely to increase the productive capacity of each economy. Without sufficient investment in energy capacity, Europe could face similar crises over the coming years.

- Political response: Europe’s energy crisis is Russia’s opportunity. President Putin is likely to use this rise in natural gas prices to extend his political ambitions. Russia was late to supply additional gas to Europe despite promising to help earlier: this was likely an attempt to support the Nord Stream2 pipeline, bypassing Ukraine and Poland to transfer gas directly to Russia. Many fear this would provide President Putin with dominance over Europe’s gas supplies. Over-reliance on Russia raises the probability of further crises.

From an investment perspective, we then note the following implications:

- REITs: Shopping centres will pay more for their own energy needs, with the impact dependent on their ability to pass this on to tenants. Energy-related expenses are generally reinvoiced to retailers (excluding common areas and vacant space). Even if we assume the sustained higher energy costs are not fully re-distributed back to retailers (50% pass through as tenants negotiate). In that case, commercial real estate earnings are significantly impacted. If you would like to access our full analysis on these companies, Carraighill Research Access allows you to access these and other thematic and sectoral research through our secure online portal.

- Consumers & retailers: Energy and vehicle costs at end 2019 represented c.10% of household consumption across Europe. This essential item is split into two areas:

-

-

- Home heating and electricity.

- Petrol and diesel for cars.

-

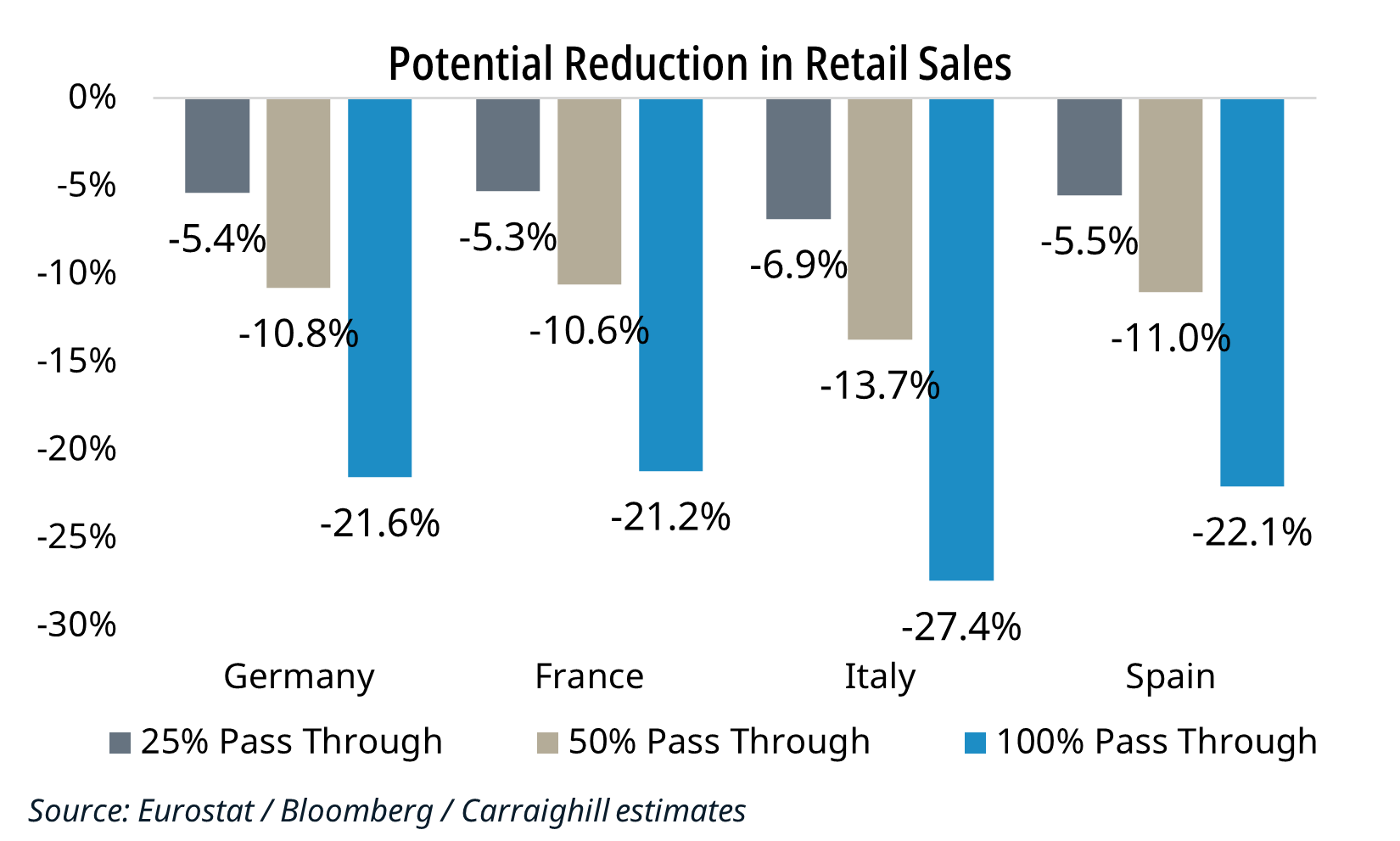

The surging costs of these two items are likely to change the composition of consumer spending. Assuming this price surge has a 25% pass-through rate, we expect non-essential retail expenditure to decrease by c.5-7% across the major Euro Area economies.

Europe’s energy crisis could hamper the economic recovery. The widespread effects of rising prices could be significant. Discretionary retail sales are likely to suffer significantly if energy prices remain elevated for a sustained period. This pressure on in-store retail is coming when the movement online was already accelerating and consumer spending was slowing. In addition, the downward trajectory of rent, which we noted previously, now faces an additional headwind.

If you would like to access our work, Carraighill Research Access enables you to access these and other thematic and sectoral research through our secure online portal. If you would like to speak to a partner or analyst on the topics raised in this piece, you can contact us here.