Corporate Interest Coverage Ratios Are Set to Collapse. Does it Matter?

The Euro Area has spent most of the past two decades in an era of low or negative interest rates, supported by quantitative easing. Non-financial corporates have been incentivised to increase their debt levels, while investors have been pushed from government bonds into corporate bonds in a search for yield. This led to three important outcomes:

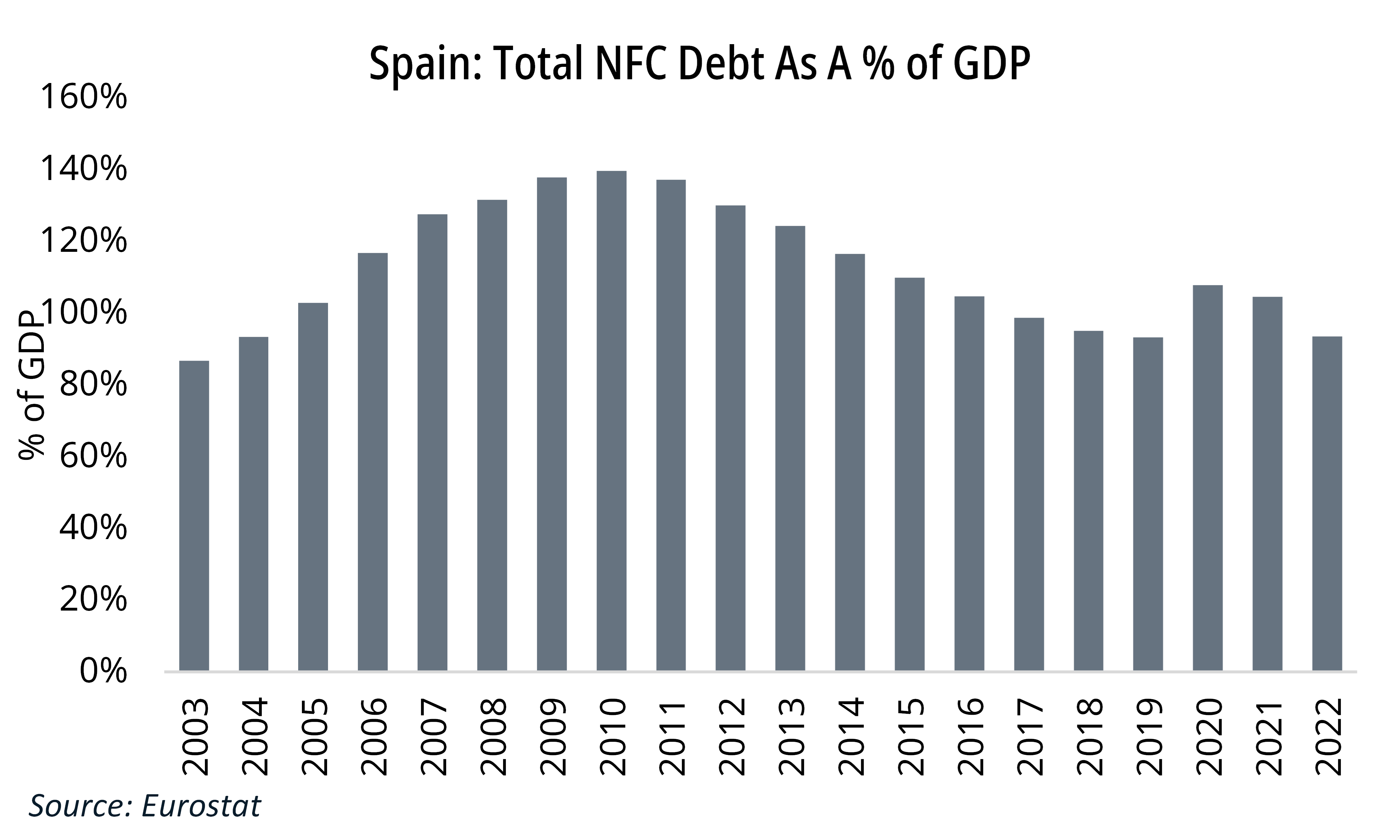

1. NFC debt increased in several European countries. In France, corporate debt-to-GDP doubled in absolute terms and went from 100% of GDP in 2003 to 162% in 2022. However, in Spain, it fell from 140% to close to 100% of GDP.

2. Domestic European banks lost market share to the bond market and non-bank and private lenders. Spain illustrates this decline as the percentage of loans held by the banks has fallen from c. 65% to 40% over the last decade. Banks lost market share while also facing lower interest rates on their remaining NFC loans. The rate charged on all loans fell.

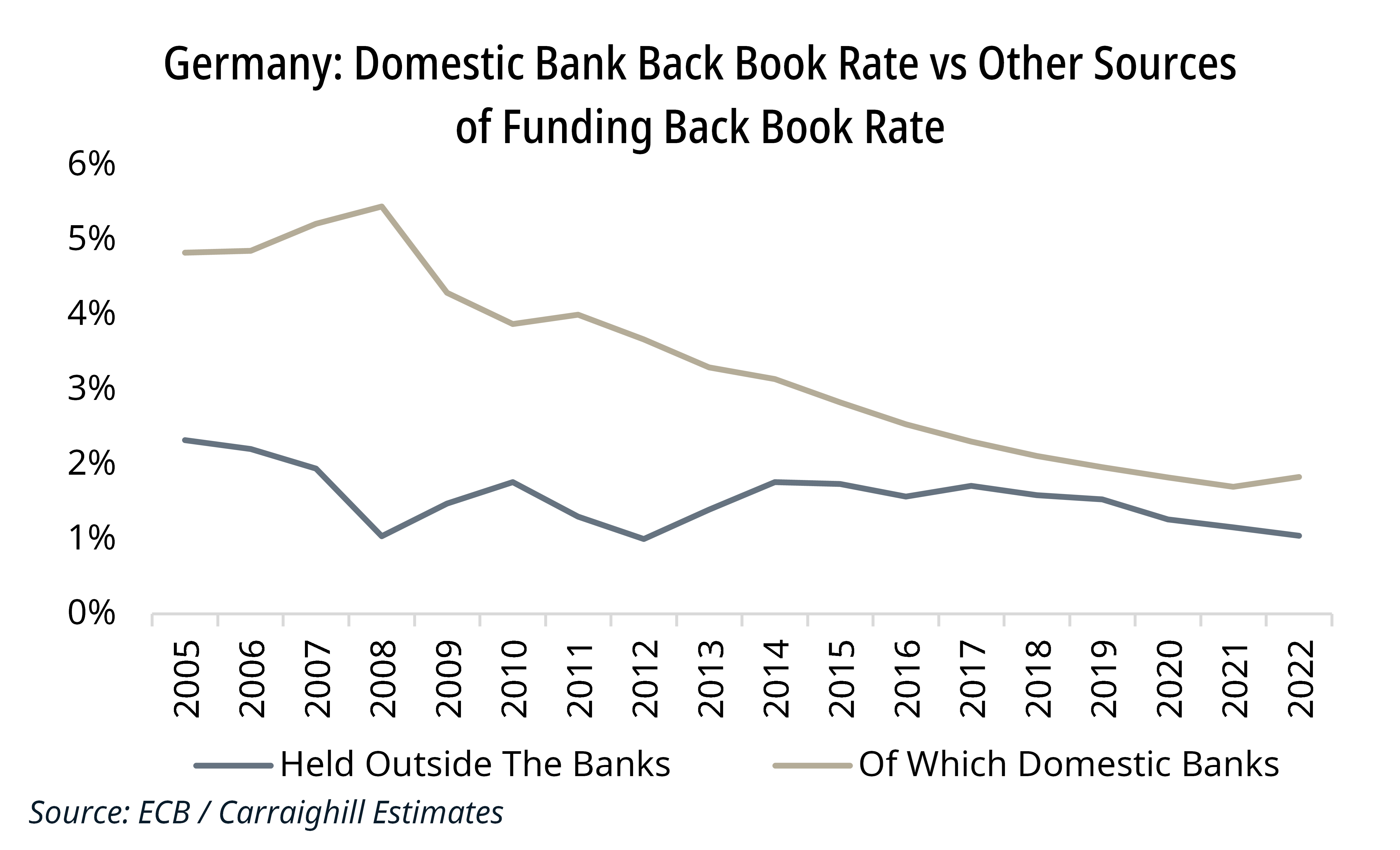

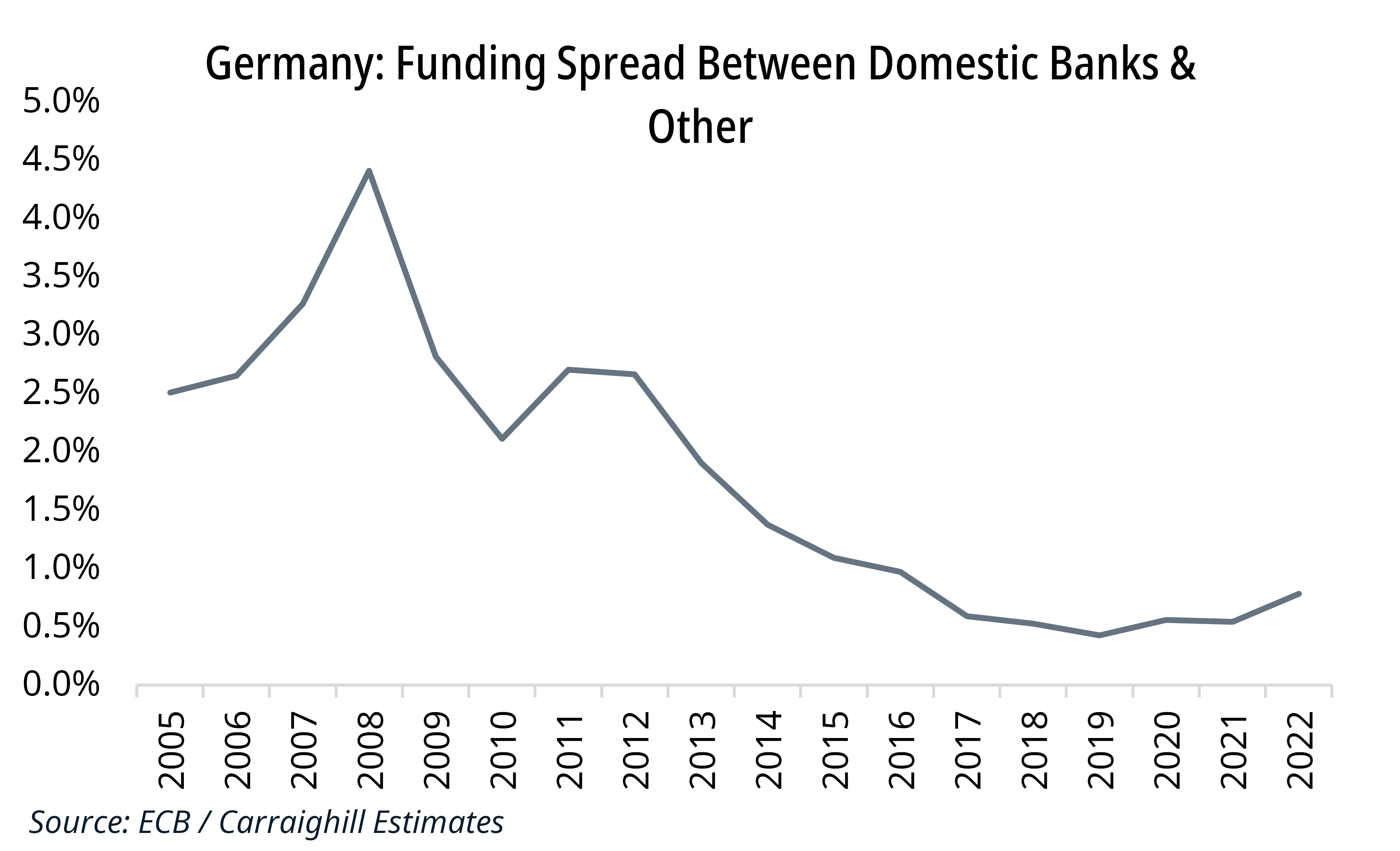

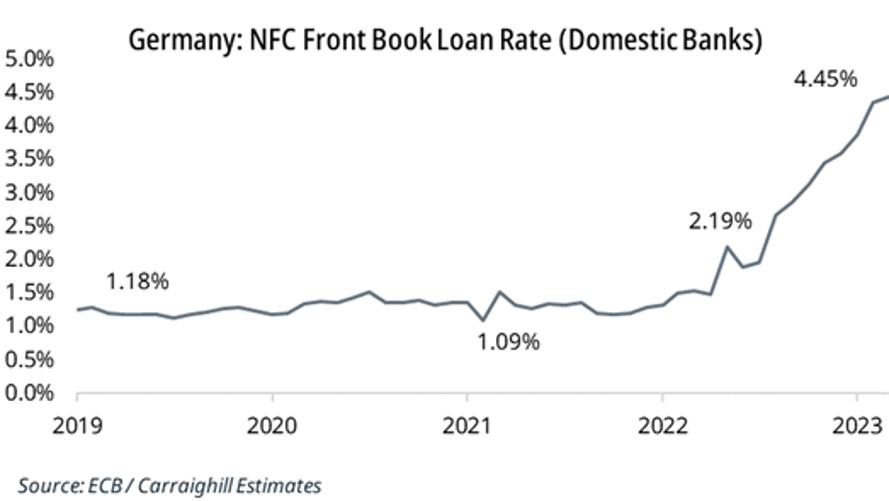

3. European bank margins compressed relative to the bond market: Bank funding normally commands a premium price. While the front book rate charged by European banks has increased markedly in recent times, the spread between a domestic bank loan and the rate charged from other sources has been structurally decreasing over the last decade. It was 2.5% in Germany in 2005 and was just 0.8% at the end of 2022. In Austria, it was 3.1% in 2005 and 0.7% in 2022. This is now changing with front book loan rates rising sharply (see Germany).

As we fast forward to today, we note that inflation has ended access to cheap bond financing. This creates rollover risk to higher rates.

Interest Coverage Ratios are Set to Collapse

We have estimated the NFC interest coverage ratio to 2025f across the eight largest European economies. We assume that the pass through takes 3 years and we consider increases in borrowing costs of 300bps, 400bps and 500bp (with an equal proportion each year). We measure NFC interest coverage as gross operating surplus over gross interest paid. The impact is profound. For example:

- Germany: The coverage ratio declines dramatically from 23.1 to 9.7 and 7.2 in 2024f and 2025f, respectively for a 300bps move. This is below the 2003 level. That said, German companies still appear in a strong position. If we increase rates by 400bps and 500bps, coverage falls to 5.6x and 4.7x respectively.

- France: NFC interest coverage drops from 4.6 in 2022 to just 2.2 in 2025f for a 300bps move. This is lower than any point over the last 20 years. France is in a particularly difficult situation as it has a higher NFC debt stock (162% of GDP vs 73% for Germany).

- Netherlands: The NFC interest coverage ratio falls from 9.2 to 5.1 in 2024f. A decline in NFC gross surplus in 2024f and high NFC debt stock are the main causes.

The investment implications are clear across the European banks and diversified financials sector.

But the credit risk is potentially not exclusive to the European banking sector this time around? The question is, who now owns the debt and who is most exposed?

This is a topic we have reviewed internally at the stock specific level as we review around 50 European banks, private equity, and asset management firms.

If you would like to access our work, Carraighill Research Access enables you to access these and other thematic and sectoral research through our secure online portal. It also gives you access to investment ideas across the banks, payments, fintech, asset management, and real estate sectors for European and select emerging markets. If you would like to speak to a partner or analyst on the topics raised in this piece, you can contact us here.